- JP

- EN

Dialogue Between Outside Directors and Shareholders

To realize the sustainable enhancement of corporate value, Mitsui O.S.K. Lines, Ltd. has an effective Board of Directors that guarantees appropriate decision-making.

This special feature presents a dialogue in which MOL's outside directors discuss their thoughts on a broad range of topics, with a focus on the Company's governance.

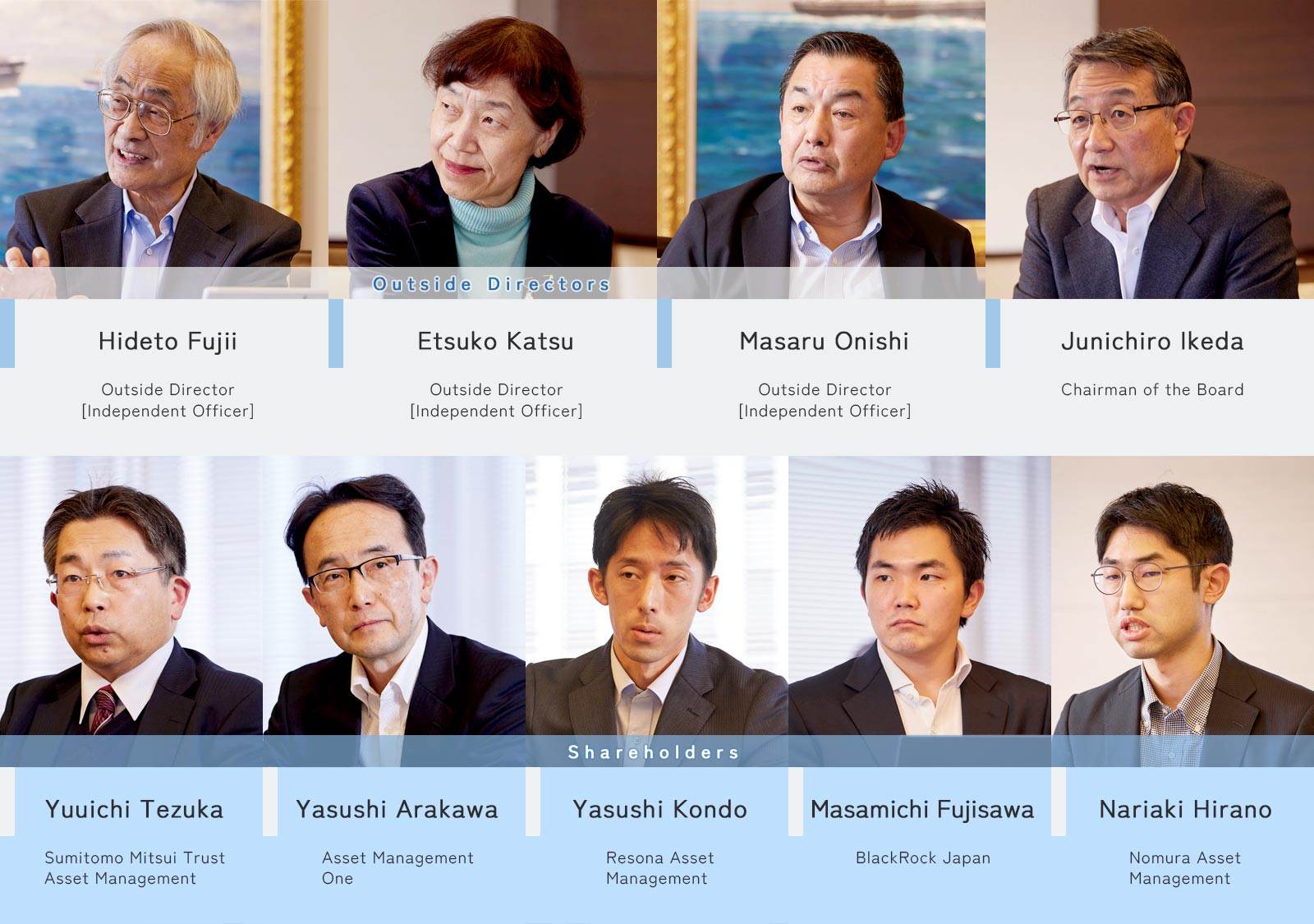

Starting in fiscal 2022, MOL has held small meetings in which the Company's outside directors and chairman of the Board engage in face-to-face dialogue and exchange views with major shareholders. At the second event, held in fiscal 2024, the participants discussed a variety of topics, including how to enhance MOL'scorporate value, strategies under BLUE ACTION 2035, and the Company's future direction. Four outside directors and MOL's chairman of the Board, Junichiro Ikeda (as of February, 2025), responded to forthright questions from five institutional investors.

MOL's Governance - An Ongoing Evolution

Noda I believe that having a lively Q&A session at a board meeting does not necessarily equate to an effective discussion. I have heard of cases at other companies' board meetings where although many questions are raised and much time is spent on discussion, it does not bring the board any closer to a conclusion. How is MOL's Board of Directors working to improve the effectiveness of its meetings?

Onishi I believe that the most distinctive feature of MOL's governance is the presence of its Corporate Governance (CG) Council, which was launched in fiscal 2021. Although some other companies have established similar bodies, I feel that many of them operate on a concept of "exchanges designed to avoid divergence" and that the discussion tends to be controlled. In the case of MOL, however, chairman of the Board Mr. Ikeda spearheaded the effort to create a forum where members could speak frankly and openly, and a year was spent discussing the concept of and building the Council. The Council was designed as a place where all directors can speak freely on any issues that come to their attention, with countermeasures to these issues then studied by the Company's other committees. When the CG Council was first launched, we invited people with senior management experience at other companies to discuss the need for changes to MOL's corporate governance system from a variety of perspectives. This type of discussion is not usually held at board meetings. It was possible because of the CG Council framework. As a result of this discussion, we came to the conclusion that MOL's current corporate governance system still has plenty of potential. This ultimately drove an evolution to its current governance structure of a company with an Audit & Supervisory Board, with nonexecutive inside directors. As the Company was able to conduct simulations based on these discussions, even if it were to change its institutional structure in the future, there would be much less apprehension or resistance to such a move.

Katsu As Mr. Onishi mentioned, in fiscal 2022 we invited external experts including lawyers to consider what the ideal governance structure ought to be for MOL, and as a result of these discussions, we all came to the conclusion that a structure which has the independence of Audit & Supervisory Board members and their right to investigate enabled proper monitoring of the Company. Even with the governance structure of a company with a Nominating Committee or a company with an Audit and Supervisory Board, largescale investments are ultimately deliberated by the Board of Directors. As MOL aims to increase the efficiency of its business operations, I believe that the current governance structure of a company with an Audit and Supervisory Committee is the most appropriate from the perspective of Board independence. Another unique feature of MOL's governance is that by appointing non-executive inside directors, it has directors with in-house knowledge who serve a bridge function between outside directors and top management. I also believe that the Company's Nomination Advisory Committee is fulfilling its role effectively. When President Hashimoto assumed the position of CEO, we thoroughly examined the role that MOL's CEO should play and the qualities that the CEO should possess, and since then these criteria have been used to update the list of potential successors on an annual basis.

Conveying the True State of the Business to Ensure Proper Assessment of Corporate Value

Tezuka From your perspective as outside directors, what are the challenges you perceive in operating the business with a firm awareness of the cost of capital and stock price?

Katsu The Board of Directors has had numerous discussions on how to achieve management with a firm awareness of the cost of capital and stock price, particularly with regard to price-to-book ratio (P/B ratio). As of February 2025, MOL's P/B ratio was approximately 0.8x, and although its stock price is trending upward, its P/B ratio has yet to reach 1.0x. On the other hand, I believe that the ¥100.0 billion share buyback program that was announced in October 2024 and the recent high dividend payout ratio have been well received by the stock market participants. MOL is being managed with a firm awareness of stock price under BLUE ACTION 2035, and I expect this approach will be emphasized even more strongly in the future.

Onishi The shipping market is characterized by its drastic ups and downs. Due to this, and also based on past performance, some people may perceive the shipping industry as a high-volatility, high-risk, high-return business. Despite such industry characteristics, MOL created its Group corporate management plan, BLUE ACTION 2035, with the resolve to build a business structure capable of generating stable profits even in times when conditions in the shipping market are weak. While the Company has been aggressively carrying out investments based on the strategies outlined in BLUE ACTION 2035 and is beginning to see results, the value of its current capabilities has been somewhat drowned out by the buoyant shipping market in fiscal 2024, making it difficult to recognize the fruits of its efforts. I believe that the true value of these initiatives is more difficult to appreciate now that the market is no longer in a downturn.

Tezuka I believe that if MOL's profitability has improved under BLUE ACTION 2035, it should have been positively evaluated by investors, resulting in a P/B ratio above 1.0x. Why do you think this traditional view of the shipping industry still persists?

Ikeda I believe that the narrative we have laid out in BLUE ACTION 2035 has been well received by investors. However, to fully convince investors, we need to deliver quantitative results, not just a narrative. To receive a positive evaluation from the stock market and by extension a P/B ratio of 1.0x or higher, I believe we must quantitatively demonstrate the benefits of each investment project once they reach full-scale operation.

Tezuka BLUE ACTION 2035 outlines MOL's strategy of increasing the spread of its unique business portfolio in the form of ROA Cost of Capital.* I believe that MOL will need to show investors within a few years that the management decisions made based on this strategy have generated stable profits, and ultimate returns. Even at the current stage, I believe that conveying some symbolic, concrete examples of the proactive investments being implemented would provide compelling evidence. Alternatively, you could show how profits from stable revenue businesses and non-shipping businesses are accumulating, leading to a stronger business portfolio and increased resilience to market conditions. I think that explaining the returns you expect from the current investments, which are progressing steadily, and the stability of these returns would help to enhance the valuation of MOL's stock price. I personally believe that MOL has outstanding capabilities in certain areas, even among its peers in the global shipping industry, and I therefore hope that you will work to bridge this "gap" in understanding with the market.

* Under BLUE ACTION 2035, MOL is also managing the financial return generated by investments using portfolio-specific ROA and ROA Cost of Capital as metrics.

Ikeda The Board of Directors carefully examines and discusses investment projects from the perspective of their potential to contribute to stable earnings in the future. However, not all investments can immediately translate into tangible results in our financial statements. Although it may take some time, we intend to present this information in a quantitative and easy-to-understand manner.

Noda I understand that it takes some time for tangible results to materialize. I would like to see MOL disclose its progress and any quantitative results at the current point in time in a transparent manner. You could add to this by proactively communicating MOL's perspective to investors. Rather than simply presenting all disclosable information and leaving it up to investors to make their own assessment, I feel it would be more effective to proactively communicate how MOL would like investors to perceive the information.

Arakawa The fact that MOL's price-earnings ratio (P/E ratio) is currently trending in the mid-single digits is evidence that it is indeed perceived as a company whose performance is linked to market conditions. While I hope that MOL will also continue to increase its P/E ratio, from an external perspective, it is always difficult to get a clear picture of what concrete plans, actions, and progress are being made at any given time. In order to increase market expectations, I would like to see MOL actively communicate how close it is to reaching the goals it has envisioned. Even if the Company places greater emphasis on ROA Cost of Capital, I believe that as long as the P/B ratio remains low, the market's evaluation of the Company will remain unchanged from the past. If the outlook for stable profit generation becomes clearer, the perception of the stock market will shift, leading to increased potential for a double-digit P/E ratio.

Human Capital is the Key to the Success of Strategies Under Implementation

Hirano MOL is currently working to reform its business portfolio in order to secure stable earnings. When approaching this challenge, monitoring progress from a financial perspective is vital. Accordingly, I believe that the Board of Directors should include members with a high level of financial expertise. What are your thoughts on this?

Onishi While I agree that a financial perspective is naturally a necessary skill set, anyone in a management position, for instance, will possess a certain degree of financial knowledge. I believe the important point is the ability to oversee management not just from a finance perspective but from a broad perspective encompassing the financial dimension, and I feel it is necessary to increase the number of members with this skill set on the Board.

Kakinuma I think that MOL's human capital is another key factor in the Company's efforts to develop new stable revenue businesses as it works to reform its business portfolio. As you work to develop new businesses, do you have any plans to strengthen your human capital or corporate divisions?

Yamaguchi In terms of human capital strategy, MOL is now developing a corporate skills matrix to identify and bridge the gap between the portfolio of its current employees and that of future ones, essential to achieving the goals set in BLUE ACTION 2035. In the process of this initiative, expertise for new business development, for example, is also considered in addition to MOL's traditional skill sets, since MOL is now widening its business frontier. MOL started the operation of its talent management system in April 2024. The system includes basic information of each employee, and has been utilized for promoting suitable candidates to key positions in MOL Group companies. Going forward, such information as performance evaluations should be added to this database. This would lead to creating a platform for enhanced human capital portfolio and optimal allocation of human resources for implementing its key strategies.

Onishi Talent management platforms developed in Europe or the U.S. are still relatively unfamiliar to Japanese companies. However, the fact that the MOL Group is not that large in terms of employee numbers makes it easier to utilize this system effectively. Thus far, MOL has been able to steadily attract key talent by strengthening its mid-career hiring initiatives. I believe that it is essential to understand what skill-and at what leve-new hires bring to the organization.

Ikeda Recently, there have also been discussions within the Board of Directors regarding strengthening the Company's corporate functions from a risk management perspective. MOL is currently working to strengthen its regional organizations in line with its Regional Strategy, and we therefore need to consider how to structure our corporate functions from a global perspective rather than just domestically. To enhance our corporate functions, we require talented people with expertise not only in developing new businesses, but also in fields such as finance, human resources, and auditing. After discussing at the Board level, we have conveyed the importance of this issue to the executive side, and it is one of our key focuses.

Yamaguchi Under MOL's Regional Strategy, the executive structure of each regional organization has been strengthened in order to expand new businesses there. This was initiated in India in 2022 as a model for other regions. Also, starting with giving a new mandates to regional offices, various measures for encouraging regional business activities are being introduced. However, it is still in the process of creating new businesses in each region, and MOL is now entering the next phase, realizing synergies by connecting "dots" into a value chain. I am certain human resources strategy is the key to achieve this.

Unwavering Determination as One of the First Movers

Noda You have declared your intention for MOL to be one of the first movers in the pursuit of a decarbonized society, but I feel that the global trend toward decarbonization has cooled somewhat, due in part to factors such as changes in the U.S. administration. Given these changes, do you still intend to remain as one of the first movers?

Toyonaga I have been involved in addressing global environmental challenges since some 30‒40 years ago, around 1989, which is often referred to as the year in which global environmental problems first came to the fore. Although I was initially skeptical about environmental issues, I came to realize through experience that companies who move first in making environmental investments are the winners, while those who lag behind face even steeper business challenges. In other words, addressing environmental issues ahead of others is in itself meaningful. When I look at BLUE ACTION 2035 from this perspective, I sense MOL's determination to move forward in a decisive manner as one of the first movers. I believe that this declaration is not merely for appearances, and that taking the initiative and forging ahead as a pioneer will lead to an increase in MOL's corporate value over the medium to long term. MOL's commitment to this challenge is firm. Although the pace and speed of its initiatives as a first mover may need to be modified in light of recent changes in the global landscape, and the fact that it is still unclear how energy sources will shift in the future, I feel that MOL's determination to pursue this goal remains unchanged.

Katsu We also discuss how MOL's first-mover initiatives relate to profitability at Board of Directors meetings. In terms of short-term profitability, I believe these initiatives may have a negative impact in some cases. However, as there are few precedents of Japanese companies serving as an opinion leader to the world, I believe that communicating MOL's stance thoroughly will ultimately serve to enhance its value in the global society over the long term.

Noda I felt that being one of the first movers was an excellent step, so although I was concerned that the Company's resolve may have been affected by the recent increase in geopolitical risk, I was relieved to hear that MOL's determination remains unchanged.

Yamaguchi While our initiatives as one of the first movers will not change, the time frame and the way we launch various measures would be evolved. Nevertheless, I am certain MOL should respond to the needs of its customers committed to decreasing their Scope 3 emissions.

Ikeda The executive side shares this determination to take the lead as first movers. Although we will be at the forefront, it is not our intention to break away from the pack and run alone. To compare our efforts to running a marathon, if we were running in the top group and the chasing group started to lag, rather than forging ahead on our own, we would remain aware of the need to pull the others along with us. Instead of accomplishing this mission on our own, we intend to build global cooperative relationships to create a new "mainstream."

Tezuka As institutional investors, we also have a longterm outlook and realize that in pursuit of this goal, it is only natural for the pace of efforts to change depending on the circumstances at any given time. I understand that the goal remains the same from a long-term perspective, but the course taken to reach the final destination may change. MOL has acted as a mover in the shipping industry since the integration of the container shipping businesses of three Japanese shipping companies, and I look forward to seeing MOL display leadership in the environmental field as well. I believe that these efforts will ultimately lead to an increase in MOL's corporate value.

- Sustainability TOP

- Message from the Chief Sustainability Officer

- Sustainability

Management - Value Creation

Stories - Environment

- Safety

- Human Capital

- Digital Transformation

- Governance

- Social Contribution

Activities - Stakeholder

Engagement - Sustainable Finance

- Sustainability Data

- ESG Disclosure

Guideline Indexes - External Recognition

- Library